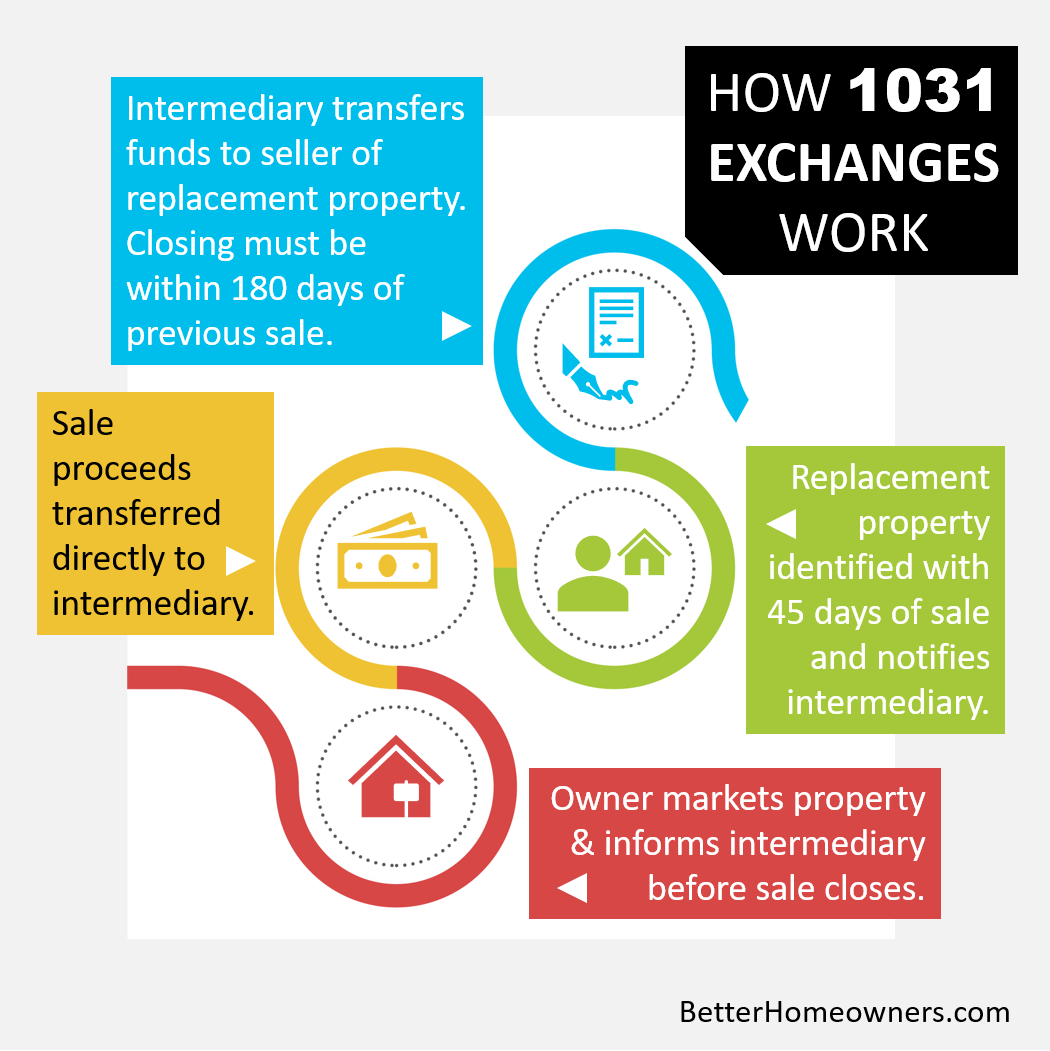

A 1031 exchange gets its name from Section 1031 of the U.S. Internal Revenue Code, which allows you to avoid paying capital gains taxes when you sell an investment property and reinvest the proceeds from the sale within certain time limits in a property or properties of like kind and equal or greater value.

It is estimated that as many as two-thirds of investment properties use this provision.

We recommend you speak with your realtor and/or tax professional to discuss 1031 exchanges whenever you intend to sell an investment property and are intending to purchase additional properties. Email us at info@soundnvest.com or call 510.377.8853 to learn more.

Ideally, each party will pay their own closing costs associated with the purchase and the sale of a home, but they can be negotiable based on lender requirements and market conditions.

The fees are usually paid at the settlement and will be itemized on the closing statement. Buyers should be aware of them before contracting for a home. If a mortgage is involved, the lender will want to verify that the borrower has ample funds available at closing to pay for them.

Buyer’s closing costs can range between two to five percent of the sales price. The real estate agents should be able to give you an estimate of what a buyer can expect. The most accurate estimate will come from the lender at the time the loan application is made. They may or may not include other fees that will be charged to buyers by the title or escrow company.

Buyers are required to be provided a standard Closing Disclosure form at least three business days before the loan closing date. This document will include the loan terms, estimated monthly payments, loan fees and other charges. This can be compared to the loan estimate provided by the lender when the application was made.

Fees connected to a mortgage

Loan origination fee … This is the lender’s fee for processing the mortgage application. It can vary in amount but typically, it can be one percent of the mortgage amount. It may be possible to negotiate this fee into the rate of the mortgage.

VA funding fee … This is a fee charged to the veteran for closing the loan. It can be paid in cash or rolled into mortgage. The amount is based on the status of the veteran, their down payment and whether they have had a VA loan before.

Appraisal … This is a fee paid for a licensed appraiser to determine the value of the property. It validates that the mortgage will not exceed the purchase price and that the buyer has enough down payment based on the type of mortgage applied for.

Attorney fee … This fee is charged to ensure that the legal documents are drawn properly so the lender will have an enforceable mortgage. It is not for legal representation of the buyer.

Discount points … A point is one percent of the mortgage. These fees are considered prepaid interest and can be used to adjust the interest rate on the mortgage.

Lender’s title insurance … This coverage insures that the lender has an enforceable lien from title claims on the property. This policy is usually issued in connection with an owner’s title policy and is priced separately.

Mortgage insurance … Most loans made in excess of 80% of loan to value require mortgage insurance to protect the lender from loss if the property must be foreclosed on. There is no mortgage insurance requirement on VA loans. FHA mortgage insurance premium has two parts. There is an up-front charge of 1.75% of loan amount and then, a monthly amount which is added to the payment. Conventional loans usually collect the first month’s premium in advance and subsequent amounts are rolled into the mortgage payment.

Recording fees … These are fees that are for filing the legal documents with the municipal or county recorders. The documents would include the mortgage and the deed.

Survey fees … This fee is necessary, based on requirements of the lender, to verify property lines, shared fences and driveways and to identify any other encumbrances.

Underwriting fee … This is a separate fee that covers the research and determination that the entire loan package meets the lender’s requirements.

Fees required by mortgage for escrow account

Property taxes … Lenders can require two to three months taxes to be held in escrow so that there will be enough to pay them in full 60 to 90 days before they are due.

Property insurance … Insurance is paid in advance and the annual premium will be due at closing. The lender further requires one additional month’s amount so that one month prior to the anniversary date, the premium can be paid for the renewal.

Flood insurance … The lender may require flood insurance on the property based on their assessment of the location in a flood zone or proximity to a flood zone.

Fees connected to purchase of a home

Settlement fee … This is the buyer’s portion of the fee paid to the title or escrow company, or attorney who handles the closing of the sale.

HOA Fee … Home Owner Association fees are usually paid in advance by the owner. They are prorated at closing for the amount paid that the seller does not benefit from.

Owner’s Title insurance … This coverage insures that the buyer, the new owner, received clear and marketable title from the seller. It will protect the new owners’ interests should they be challenged. Even though it may not be required, it is recommended.

Pest inspection … A pest inspection by a licensed exterminator can be required by a buyer to determine if there are active termites or termite damage, dry rot or another pest infestation.

Property inspection … A home inspection conducted by a professional can be required to determine structural integrity of the property as well as all the systems in the home. It can include but not be limited to plumbing, electrical, roof, heating and air conditioning, appliances and other things.

Title search … Sometimes, title companies waive this fee when an owner’s title policy is issued. It can be customary that a separate fee is charged in addition to the premium for the title insurance.

Transfer taxes … When government taxes are required, these fees must be collected.

The Consumer Financial Protection Bureau is a U.S. government agency that makes sure banks, lenders and other financial companies treat the public fairly. You can download a Closing Disclosure Explainer from their website.

Debt-to-Income ratio is a tool that lenders use to qualify buyers for a mortgage and is an important factor in determining loan approval. It provides an indication of the amount of debt that a potential borrower is obligated to in relation to how much income they have.

Total monthly debts are determined by adding the normal and recurring monthly debt payments such as monthly housing costs, car payments, minimum credit card payments, personal loan payments, student loans, child support, alimony, and other things.

By dividing the monthly income into the monthly debt, you arrive at a percentage of the monthly income. Lenders actually look at two different ratios commonly called the front-end and the back-end.

The front-end ratio is the proposed total house payment including principal, interest, taxes, insurance, mortgage insurance if required, and homeowner association fees. Lenders generally don’t want these expenses to be more than 28% of the monthly gross income.

The back-end ratio includes the same items that are in the front-end ratio plus any other monthly obligations like the ones mentioned earlier. Lenders prefer to see this ratio not to exceed 36% of monthly gross income but some lenders may extend that to 43%. Borrowers obtaining an FHA mortgage might also be allowed an even higher back-end ratio.

If a borrower had $8,000 monthly gross income, their proposed house payment should not exceed $2,240 or 28% of their monthly gross income. Then, their house payment and monthly debt should ideally not exceed $2,880 or 36% of their monthly gross income.

For the sake of an example, let’s say that their monthly debt was $900. That would only leave $1,980 for the maximum house payment. The monthly debt became a limiting factor affecting the house payment.

In addition to determining whether the buyer qualifies for the mortgage, it could affect the interest rate. Having good credit and having the proper ratios can result in being approved for a mortgage. On the other hand, if the debt is on the upper side of an acceptable range, the lender may charge a higher interest rate for the addition risk of a marginal borrower.

While the math is not difficult to come up with your ratios, it is not necessarily a do-it-yourself project. A trusted lending professional can assess your situation and give you an accurate picture of what price home you can afford and the rate you can expect to pay.

Both things are important to know before you start looking at homes and especially before you contract for one. All lenders are not the same. Call me to get a recommendation of a trusted mortgage professional who specializes in the type of mortgage you want. Download this FREE Buyers Guide.

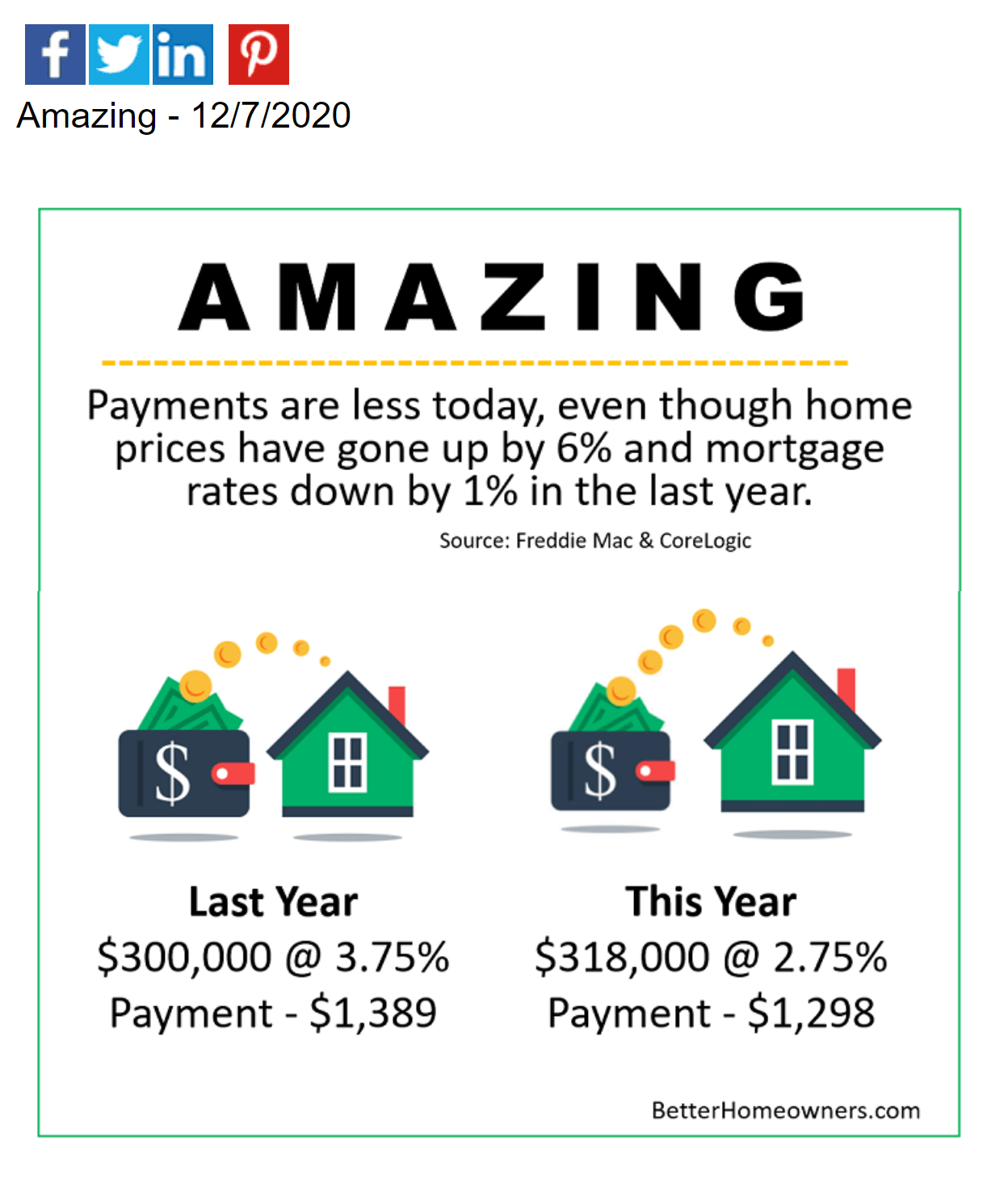

If for whatever reason you decided not to buy last year, you may actually be better off now. As you can see, even though a property may have increased in price by 6%, with interest one percentage lower, your total and monthly payments may actually be lower.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Rolanda Wilson and Better Homeowners do not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Rolanda Wilson and Better Homeowners. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Selling a home and buying a lower priced home that meets your current needs can be to your advantage in an “Up” market like the current one with low inventory. The advantage is that you can maximize the price for the home you’re selling and not have to reinvest it all in your replacement.

Just to illustrate the point, let’s say there is a 10% premium in the sales price of a home currently. If you’re selling a home for $750,000, it would be $75,000. If you replaced the home with a $500,000 home, the premium would be $50,000 which means you’re $25,000 ahead.

Let’s further assume that your home is debt free so that when you sell it, you have a large cash equity. Instead of paying cash for the replacement home, get an 80% loan at today’s low interest rates and reinvest the proceeds to supplement your retirement.

You may be able to get as low as a 2.5% mortgage and earn significantly more on the proceeds in other investments.

Home prices are up significantly over last year and they’re selling on average in three weeks. Inventory is down and there is less competition for your home than normal which can lead to a higher price. Closed sales increased 9% from August to September according to a Zillow report.

Moving down in an “up” market may be to your advantage. It could lower your cost of housing by saving on property taxes, insurance, utilities and maintenance while being able to take cash out of your home to reinvest in your retirement.

You’ll be using “other people’s money” to free up your equity that you can reinvest at a rate higher than you’ll be paying on your mortgage. The difference would be profit.

To explore this opportunity, give me a call at 510.377.8853, and we’ll look at your numbers.

Up to $500,000 of capital gain on the sale of their home for couples filing jointly and $250,000 for single filers is excluded from income tax if they own and use it as their principal residence for 2 of 5 of the previous years.

Banks are concerned about making loans that will be repaid not about making loans that are tax deductible for homeowners. It is good business for the bank but how is the homeowner supposed to know?

Most homeowners and potential homeowners are aware there are tax benefits associated with ownership. For instance, mortgage interest and property taxes have been deductible expenses from federal income tax since it was enacted in 1913.

The current law provides that homeowners can deduct the interest on Acquisition Debt which is the amount of debt incurred to buy, build or improve a first or second home up to $750,000. The amount of acquisition debt decreases as payments are made and it cannot be increased unless the additional funds borrowed are used for capital improvements.

It is not uncommon for a homeowner to refinance their home for any number of reasons. It could be to get a lower interest rate that would lower the payments or remove mortgage insurance. However, when additional funds are borrowed for reasons beyond “buy, build or improve”, the excess is considered personal debt and the interest is not deductible according to IRS.

Maybe this is not important if the owner is taking the standard deduction because it is higher than the total of the property taxes, qualified mortgage interest and charitable deductions made by the taxpayer. Currently, it is estimated that 90% of homeowners are electing to use the increased standard deduction implemented with the 2017 Tax Cuts and Jobs Act.

A confusing issue that occurs at the end of the year is when the lender reports to the borrower the amount of interest that was paid. While that amount is most probably accurate, the bank doesn’t know if it is qualified mortgage interest for the borrower.

It is the responsibility of the taxpayer to keep track of outstanding acquisition debt and whether part of the balance is considered personal debt.

Another area where it could become important is if the property was lost due to foreclosure, deed in lieu of foreclosure or a short sale. The provisions of the Mortgage Forgiveness Act have been extended through 12/31/20 which exempts the forgiven debt from being considered income and therefore taxable. However, it only applies to acquisition debt. Any part of a mortgage refinance that is considered personal debt could be taxable in that situation.

As an example, let’s say that homeowners originally borrowed $300,000 to purchase a home that they owned for 15 years. During that time, the home appreciated significantly, and they refinanced it twice. Once, they made some improvements and took out cash to pay off personal loans and the second time, it was only a cash out.

Original acquisition debt: $300,000 Remaining acquisition debt including improvements: $225,000 Unpaid balance on current mortgage: $550,000 Personal debt: $325,000

In the example above, the personal debt of $325,000 would be considered income on foreclosure and recognizable as income on that year’s income tax return.

If you have never refinanced your home or have refinanced it but never taken any money out of it except to make capital improvements, your unpaid balance in most likely acquisition debt. However, it you have refinanced your home and pulled money out of it for purposes other than capital improvements, those funds may be considered personal debt.

This article is for information purposes. If you are unclear about the current acquisition debt on your home or need advice for your individual situation, contact your tax professional. Additional information can be found in IRS Publication 936, Home Mortgage Interest Deduction.

Just like buyers should be pre-approved before they begin to look at houses, Sellers should have their home pre-approved. The reasons are similar: appeal to the “right” buyers, discover issues with the home early, improve marketability, increase negotiations position and close quicker.

For the seller, there are few things that need to be done before the sign goes in the yard and definitely before prospective buyers see the home. The first is to understand that once you decide to sell the home that it needs to appeal to the broadest base of buyers and that means depersonalizing your home.

Once the home is sold, you will need to pack your things for the new home. Think of this as starting the process early. Get moving boxes and make decisions on what you intend to give away or discard in each room and closet. Identify and pack those items before the home goes on the market. This will be the first wave of making your home more marketable.

When your home hits the market, it needs to be a neutral commodity and not “your” home. A good rule of thumb is to remove items that involve religion, hunting and sports. That means removing personal items like family photos or collections displayed in the room.

Next, in round two, go through every room to remove the items that make too large of a statement or take up too much room. Pool tables may be appropriate in a game room, but they are not in a dining room or a living room.

Personal collections may have taken you years to accumulate and you’re proud of them but the people who come to see your home will either not appreciate them or they will become distracted by looking at them instead of the home. The livability of your home needs to be the focal point. The buyers need to visualize themselves living in the property that will become “their” home.

The four most important rooms to address are the primary bedroom, kitchen, living room and dining room. These rooms have a major influence on buyers when determining whether “it is the right home.” Bright colors, possibly used as accent walls, should be neutralized.

After you have depersonalized the home and removed non-essential items that could make the rooms or closets look small, you might want to consider another technique referred to as staging. Rearranging furniture so the room shows to its best advantage is simple and doesn’t cost a thing. You might decide that a coffee table or statement piece would be nice and your realtor or stager can suggest a place to rent it rather than buying it.

Once the home is depersonalized and staged, you are ready to have a professional photographer take the pictures that visually describe your home to potential buyers long before they ever look at the home physically. These will be used on websites, portal sites, MLS, and social media. Anyone with a point and shoot camera thinks they are a photographer but a pro with the correct wide angle lens, who understands lighting and has an “eye” for what makes a great picture is worth every dime you’ll spend.

One more consideration should be to have the home inspected before it goes on the market. It won’t replace the buyer’s inspections but it will discover any items that need repair and they should be done before the home goes on the market. This will probably save you money because it might cost less to repair them than they’ll want in second round of negotiations when their inspector finds it.

Another benefit is that if their inspector identifies a problem area that your inspector did not, you have a basis for legitimate disagreement that could just be personal opinion instead of a “fact.”

While the process of depersonalizing should take part before you put the home on the market, you’ll want you have the benefit of your real estate agent’s experience to help you with the process. At age 18, a person can expect to move nine more times but by age 45, they may only expect to move another 2.7 times. Your realtor’s experience can be valuable not only in saving your time and money but actually, make the difference in a successful sale.

The concern today when putting your home on the market should not be whether you’ll get a contract; it’s whether you are going to recognize the majority your net proceeds without any unnecessary delays.

What you realize from the sale of your home has to do with maximizing the sales price while minimizing the sales expenses. Interestingly, the buyers will be trying to minimize the price they have to pay for your home and possibly, have you pay some of their expenses.

Taking a few pictures with a cell phone and putting a sign in the yard may be enough to get a buyer but successfully selling a home in today’s market requires expert marketing and expert negotiations.

Marketing begins with the preparation of the property to optimize the first impressions it makes to potential buyers. A skilled professional can make recommendations that can help the home sell for the most money and in the shortest amount of time. Cleaning, painting, depersonalizing, removing unnecessary items and possibly staging are a few of the recommendations you might receive.

93% of buyers rely on the Internet to search for properties and information and is something they engage even before they find an agent. Positioning the home so it only can be found effectively in the search is making it appeal favorably and requires careful consideration.

Professional-level photography will make the property look appealing. Experience knowing the right angles, the proper lighting, and having the right lens are only a few of the things can make a property stand out from the competition.

Negotiations plays a huge part in the sale of any home. There will be negotiations during the offer/contract stage with the buyer and the other agent. After that, there may be negotiations regarding inspections, repairs, the appraisal, or anything that might threaten the ultimate closing.

The following are seven questions that you can ask when interviewing an agent to market your home. The answers should help you evaluate and select an agent who can represent you and your interests.

1. Do you use a professional photographer? 2. Have you sold homes in this area recently? 3. Explain your timetable for preparation, “going live” and market exposure. 4. Describe your efforts during the negotiation process. 5. Do you have a pricing analysis, showing actives and solds, for my neighborhood? 6. Which properties will be our strongest competition? 7. How do you get the most exposure to get competing offers?

On the surface, it may appear that all agents are the same. They are all be licensed to sell real estate and can put your home in the MLS for other agents to find. Experience and skill sets can vary widely among agents and the questions provided in this article can help you determine who can do the best job for you in today’s environment and the market your home is located.

Is It Better to Pay Down Your Mortgage Faster or Invest? excerpted from apartmenttherapy.com

by Liz Steelman

It is a fact that you could save significantly on interest by paying a little bit more towards your principal over the scope of your home loan. However, it is also true that instead of paying more toward your principal, you may benefit more by investing that same money. For example, if the interest rate on your mortgage is 5%, and the current 30-year market growth rate for a portfolio of investments is around 8%, then you should invest that money instead of paying down your mortgage faster.

Let’s look at how this using some very simple numbers: If you have a $300,000 30-year, fixed-rate mortgage at 5% interest and you commit to paying an extra $100 every month, you’ll save nearly $40,000 in interest over the term of the home loan. However, if you opt to put that $100 monthly payment into an investment that compounds annually with an 8% rate of return of 30 years, you’re likely to end up with $140,855 when your mortgage ends. You will, however, have to pay the extra $39,937.25 on your mortgage by forgoing the extra principal payment. So your actual return will only be around $100,000. However, that still is considerably more than $40,000. This, however, is a simplistic look at the concept, but it gives you an idea on what the rate of return of investment could be.

Financial experts note that it is always a smart idea to look at the spread (the difference between the two interest rates) between what you could get through investing versus your mortgage rate (which drives what you can get early-paying your mortgage). However, these days an 8% return on investment is a little more aggressive than reality. Additionally, investment rate of return usually doesn’t include tax considerations—which can affect your rate of return (since mortgage interest is tax-deductible. Additionally, the investment timelines for portfolios with 6-8% return are usually long-term return rates. So consider how long you have left on your mortgage and compare it with the term required by your investment.

On top of that, investment rates are not often guaranteed. And, if you do earn slightly more with an investment, the freedom and peace of mind that comes with paying off your mortgage early may be priceless.