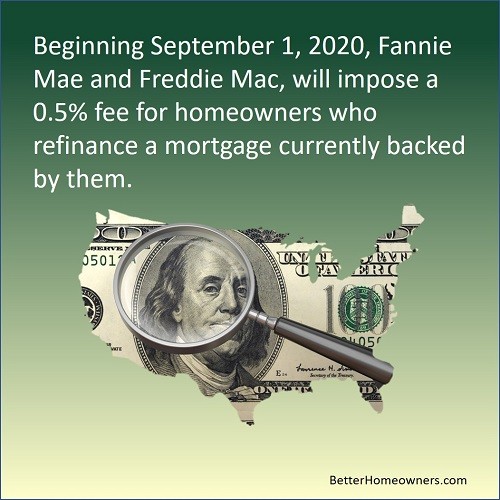

If you’re in the process of refinancing currently, see if you can close before this goes into effect.

We have the keys to your financial success.

If you’re in the process of refinancing currently, see if you can close before this goes into effect.

Want to quickly and easily improve your property’s drive-up appeal? Simply paint the front door a distinctive but coordingating color to make it pop for a more welcoming feel.

This is impoartant because without street appeal, some people may never want to see the inside of your property based on what the outside looks like.

Three reasons to refinance a home include lowering the cost of housing, shortening the term of the mortgage to pay it off sooner or to using the equity to accomplish another purpose.

Replacing the mortgage at a lower interest rate, which is entirely possible in today’s market, would reduce the payment. On the other hand, shortening the term of the mortgage could make the payments increase but would allow the home to be paid for sooner. In either case, the equity would not be reduced unless the refinancing costs were rolled into the new mortgage.

Refinancing the home to take money out would increase the mortgage on the property and lower an owner’s equity; careful consideration should be made before doing so.

Mortgage rates are considerably lower than credit card rates and usually lower than short term borrowing like student loans or car loans. For that reason, homeowners will sometimes refinance to payoff higher cost debt.

Some people refinance for more than their current balance to improve their cash position, possibly, to have funds available in case they need it. Other reasons could be to use it for an investment such as rental property or other things. Still others may use it to make capital improvements on their home like remodeling or a pool.

Another legitimate reason to refinance may be to combine a first and second lien on the home that might result in lower payments and a savings in interest.

One more situation that causes a person to refinance a home is to remove a former spouse or co-borrower from the existing mortgage. In the case of a divorce, a couple may no longer be married and one of the former spouses may have no financial interest in the home any longer but because they signed the note originally, they are still liable along with the other spouse. This could be an untenable position.

There can be a lot of reasons that cause a homeowner to refinance the home. The equity is a valuable asset that has powerful borrowing power combined with the good credit and income of the homeowner. A Refinance Analysis can help you to determine the new payments and how long it will recapture the cost of refinancing.

For the recommendation of a trusted lender, give me a call at (510) 244-0085.

You know what they say about first impressions…you never get a second chance. Take the time to make some finishing touches before your home is going to be shown.

Remember, the better your home shows, the higher the value you can ask for.

Lower interest rates amortize faster than higher interest rate loans, so you not only end up paying less over time, you pay it off more rapidly.

Forbearance is a temporary postponement of mortgage payments. The lender can grant this option to a borrower instead of forcing the property into foreclosure. The CARES Act provides protections for homeowners with mortgages that are federally or Government Sponsored Enterprise backed or funded such as FHA, VA, USDA, Fannie Mae and Freddie Mac.

A mortgage holder should contact the lender to explain the temporary difficulty they are having making payments and ask for relief under forbearance or other options. Once the lender grants approval, it is important for the borrower to get the terms of the forbearance agreement in writing to be clear about when the payments will resume and how the missed payments will be recovered.

Generally speaking, homeowners in a forbearance plan will not incur late fees and it should not adversely affect their credit. Unfortunately, borrowers must be vigilant to see that the lender is protecting them from delinquent credit marks according to their agreement.

Forbearance is easy to receive but not so easy to recover from. Free credit reports can be obtained on a weekly basis until April 21, 2021 at www.AnnualCreditReport.com. Reports are available from Experian, Equifax and TransUnion. This will allow borrowers to monitor whether the lender has inadvertently reported items inaccurately.

Prior to the end of the forbearance period, borrowers should contact their loan servicer, the company that accepts their payments. Review the terms of the forbearance plan and expectations for repayment. Verify the unpaid balance and that there are not any payments marked as late or delinquent during the forbearance period.

One more item to discuss with the loan servicer is the payment of the property taxes and insurance. Since multiple mortgage payments may have been missed and most payments include 1/12 of the annual amounts for these items, there may not be enough to pay for them when they become due.

Since it is estimated that there are over four million borrowers in forbearance currently, it may be difficult to talk to the servicer but starting the process early and being persistent will be helpful.

At the end of forbearance, the borrower needs to resume regular payments and establish a plan with the lender to repay the missed payments. The terms are negotiated between the borrower and the lender.

One way is through a loan modification which can restructure the loan. In some cases, it would add the missed payments to the loan balance and recalculate the payments for the remainder of the term.

A borrower could pay the forbearance money in cash but the practicality of that is not realistic. If the person couldn’t make the payments during forbearance, they probably don’t have the liquidity to pay them afterward. This option is entirely at the buyer’s election.

Forbearance is a temporary way to postpone the mortgage payments with the understanding that you will be able to resume repaying the loan. If the circumstances that caused the issue initially become permanent, then, other remedies must be considered. If there is equity in the property, selling the home may be the way to materialize it for the homeowner.

Please contact us at (510) 244-0085 if you need to know what your home is worth and how long it would take to sell it. We’re happy to provide this information as a service without obligation so you can be aware of your options.

Hopefully, you’ll never have to deal with losing a home to another buyer and these tips might make the difference.

by Eman Hamed February 2, 2018

excerpted from Mashvisor.com (Click here to view the entire article)

In a traditional real estate transaction, sellers and buyers rely on real estate agents to find potential real estate investment properties and close the deal. However, some sellers forego the help of an agent and do a For Sale by Owner (FSBO for short). Many follow this approach because they enjoy benefits like not paying commission to the real estate agents, making their own decisions, and having more control of the sale process.

Despite these benefits, for sale by owner has several disadvantages as well. It is important that real estate investors, or other property owners, know these drawbacks and consider them before making such decisions. Below are five disadvantages of for sale by owner and selling investment properties yourself.

For Sale by Owner Disadvantage #1: No Professional Help

Typically, real estate agents charge 4%-6% of the sale price as a commission. The fact that real estate investors don’t have to pay this commission to a real estate agent when selling homes as FSBO is perhaps the only advantage of this approach. However, property owners are not as well informed as real estate agents. If you are a first-time seller, you’ll make a number of mistakes when doing for sale by owner,which could be avoided with the help of a real estate agent.

Seller real estate agents pretty much do all the paperwork regarding a real estate transaction from start to finish. A real estate agent helps you review sales offers, write counter-offers, etc, which otherwise you would have to do on your own or hire a real estate attorney. In addition, some for sale by owner sellers make the mistake of overpricing the investment property. Meanwhile, the real estate agent has experience in how to correctly price investment properties.

Not only that, but a real estate agent will also help real estate investors in preparing and showing the investment properties to potential buyers. For sale by owner sellers may not be available for a showing when a buyer is, which limits the property’s exposure and hinders the sale process. Therefore, the best thing to do is to work with a real estate agent who will take care of coordinating open houses, schedule appointments with other agents, meet with potential buyers, and conduct showings of the property.

Moreover, according to the National Association of Realtors, for sale by owner sellers lose 28% of the price they could have gotten if the property owner worked with a real estate agent (taking commission into account).

For Sale by Owner Disadvantage #2: Less Knowledge of the Real Estate Market

The second most important reason why you shouldn’t consider for sale by owner is related to your knowledge of the real estate market. Most property owners and sellers (especially first timers) don’t have the sufficient knowledge and experience in the real estate business that ensures a successful sale. Moreover, some are not good at negotiations or don’t possess the knowledge and skills to smoothly and successfully close the transaction, which means they could be taken advantage of. Some real estate agents don’t even deal with for sale by owner sellers as they prefer working with another professional agent. If you’re not knowledgeable about the real estate market, don’t do for sale by owner!

In addition, first-time for sale by owner sellers don’t know how to correctly conduct a real estate market analysis that helps in pricing the investment property. Some just assume that because an investment property was recently sold for $200,000, then this is also their home’s worth. This is not necessarily accurate. When selling an investment property as for sale by owner, conducting a real estate market analysis is a must. However, conducting a real estate market analysis is not an easy process for those with insufficient knowledge or experience in the real estate business. You don’t want to overprice the property (which leads to getting fewer offers), and it’s obviously not to your advantage to underprice it.

For Sale by Owner Disadvantage #3: Limited Marketing

Another disadvantage of being a for sale by owner seller is that, unlike real estate agents, most property owners have limited contacts. As a result, marketing can be very challenging. Having limited contacts means you won’t be able to expose the investment property to a large number of people and attract as many potential buyers as possible. In addition, marketing and advertising can be very expensive. Listing your property on FSBO.com or Zillow.com with some pictures doesn’t necessarily result in getting good offers.

On the other hand, real estate agents have access to the best marketing technologies that are not available to average real estate investors or property owners, such as the Multiple Listing Service (MLS for short). Only licensed real estate agents have access to and can list investment properties for sale on MLS. Buyers’ agents search the MLS for potential investment properties to show their clients. For sale by owner sellers only have a few options to attract potential buyers, and, as a result, will miss out on showings. This single real estate tool can foster interest in the investment property, result in more showings, and lead to a faster sale. Unfortunately, it’s not available to for sale by owner sellers.

For Sale by Owner Disadvantage #4: Time-Consuming

Based on all the responsibilities of real estate agents which we’re previously mentioned, you can clearly tell that the traditional process of selling investment properties is time-consuming. For sale by owner takes much more time and effort! Simply putting up a for sale by owner sign is not nearly enough to get the property sold. Real estate investors need to check and inspect the investment property for anything that might need repair, prepare and stage the property, market and advertise it, handle all the paperwork and showings, and not to mention spend the time to learn how to conduct a market analysis and familiarize themselves with all legal and financial issues. For sale by owner sellers must be prepared from start to finish!

For Sale by Owner Disadvantage #5: Attachment to the Property

Finally, the for sale by owner process can be emotionally difficult for real estate investors who are attached to their homes and could have a hard time letting them go. This is, in fact, a reason why property owners overprice their investment properties when selling them as FSBO, as for them their homes are obviously very valuable. Moreover, it might be awkward for you to show your home to a potential buyer (who essentially is a stranger). Some property owners even change their minds at the sudden realization that they’re going to lose their home with all the memories it holds! For this reason, working with a real estate agent guarantees a successful real estate transaction.

Thus, before you sell your investment property as for sale by owner, consider the following questions: for sale by owner

The Bottom Line

Real estate agents are very helpful in a real estate transaction as selling a property is a complex process, and it can be overwhelming for property owners following the for sale by owner approach. FSBO will definitely allow you to save more, but you can lose the offers and potential buyers that a real estate agent will guarantee. In addition, real estate investors learn more about the real estate business by working with a real estate agent.

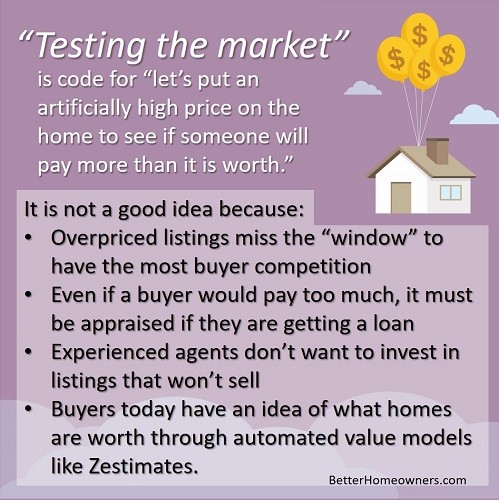

If a home is priced right in the beginning, especially while there is low inventory, competition can drive the price above list price.